Other Post-Employment Benefits Reporting (OPEB)

Table of Contents

Frequently Asked Questions

Frequently Asked Questions

What is OPEB?

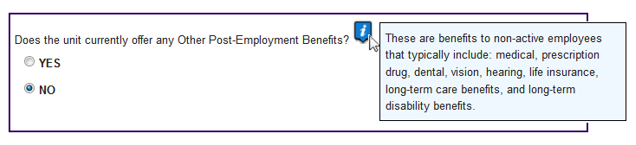

Other Post-Employment Benefits (OPEB) are those benefits that may be provided to employees after employment ends. Those benefits are separate from the normal pension offered by a governmental unit. OPEBs may include medical insurance, prescription drug, dental, vision, life insurance, long-term care benefits, and long-term disability benefits.

Why are some fields grayed-out and unavailable for data entry?

Certain fields are made unavailable based on the response to questions in step one. If a unit has not completed an actuarial valuation, the fields on the valuation are unavailable. If a unit selected the option to not report supplemental information, the supplemental questions are unavailable.

Is this a new reporting requirement?

This report was first submitted in 2014 to cover 2013 information. According to I.C. 36-1-8-17.5, each political subdivision must report information and data on its retiree benefits and expenditures by March 1 of each year.

The only post-employment benefits we offer is allowing our retirees to purchase health insurance on the group plan. However, we require our retirees to pay the full cost of their post-employment premiums. Do we have an OPEB liability to report?

It depends. In most cases, retirees pay the same premiums as active employees. This can create an OPEB liability since it increases the overall risk of the plan. The true cost for retiree health coverage is almost always higher than the cost for active employees. The retirees are older and more likely to require health care services. For example, if priced separately, the cost for a retiree health insurance plan may be $10,000 per year and the cost for an active employee is $6,000 per year. However, if priced in one large pool the price per plan would be $8,000 per year. Then, there is an implicit subsidy of $2,000 per year for each plan that is offered. The total amount of the subsidy is a part of the OPEB liability and expenses that the employer must report.

Are we required to “pre-fund” these benefits?

Not at this time. No cash contribution is currently required and no amount is required to be budgeted for this potential liability. However, some units may decide it makes sense to pre-fund OPEB’s as some units have done for pension liabilities.

If we determine that our unit does not have an OPEB liability, are we required to report anything in Gateway?

Yes. Units with no liability are still required to report and submit an OPEB report in Gateway.

Accessing the Other Post-Employment Benefits Report

Accessing the Other Post-Employment Benefits Report

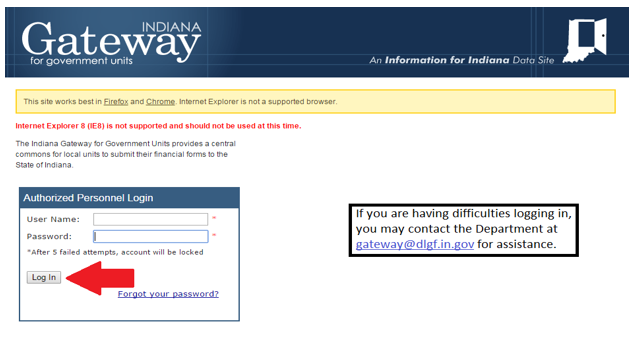

The Gateway login page can be accessed through the Gateway public data output site at

gateway.ifionline.org. Once on this site, please select the “Local Officials: Login Here” link on the top right-hand side of the page.

This will take you to the login page below. Please enter your username which is typically your email address and your password. Once done, please select “Log In.”

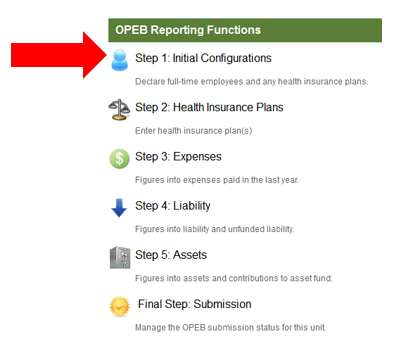

Once you have logged in, you will be taken to the Select Application page in Gateway. Please select, “Other Post-Employment Benefits Report”.

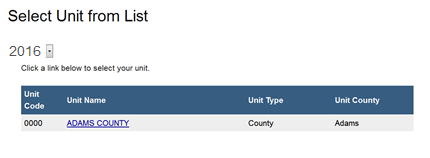

You should now be on the Select Unit from List page. Select the name of your unit to continue.

Upon clicking the name of your unit, you will be taken to the Unit Main Menu. To begin the report, select “Step 1: Initial Configurations.”

Navigating the Report

Navigating the Report

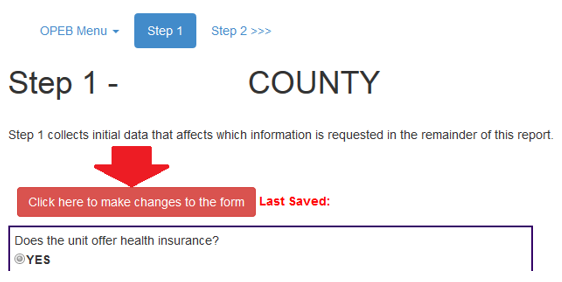

The OPEB report is organized into multiple steps. To begin entering information into most steps, please click the red, “Click here to make changes to the form” button, on the top left-hand side of the page.

Throughout the report are blue “i” information icons. Moving your cursor over these icons will reveal additional information regarding the adjacent question.

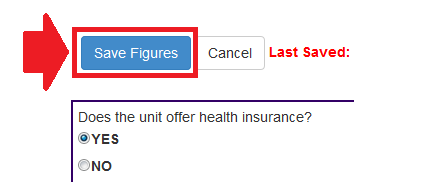

When a step is completed, please be sure to click, “Save Figures” to ensure all data has been saved.

The next page can be accessed by selecting the next step on the top left-hand side of the page.

Step 1 – Initial Configurations

Step 1 – Initial Configurations

Step 1 collects initial data that affects which information is requested in the remainder of this report. This data rolls over from what was reported the previous year.

Units without Other Post-Employment Benefits

Units that do not offer any other post-employment benefits are able to skip to submission after completing Step 1. After answering the questions, it is important to click “Save Figures” to save the currently entered data. For units without OPEB, upon saving, a “Skip to Submission” button will appear at the top of the page. This will redirect the user to the final submission portion of the report. Please navigate to the “Signing and Submitting the Report” section of this user guide for assistance submitting this report.

Units with Other Post-Employment Benefits

As questions are answered in Step 1, the remainder of the report will be customized to fit the unit’s needs. For units that offer other post-employment benefits, there are two separate paths for this report.

Units that have completed an actuarial valuation

The first path is for users that have recently completed an OPEB valuation under standard 45 of the Government Accounting Standards Board. The Department understands that some units may not be required to complete a valuation annually or that a valuation for 2016 may not be completed before the March 1 deadline. Therefore, the Department will accept a valuation completed within the last 5 years. If an actuarial valuation was completed, but there are significant changes to the plan liability, users will need to describe these changes. For units that have completed an actuarial valuation, the users may choose to enter the five statutory data points in Steps 3, 4, and 5. Users have the option of completing additional information, but is it not required for units that have completed an actuarial valuation.

Units that have not completed an actuarial valuation

The second path is for users that have not completed an actuarial valuation of OPEB. For these users, the Department will collect qualitative data and will allow users to estimate some of the information typically calculated in an actuarial study. The Department understands that these will be estimates and the Department acknowledges that users who elect to enter these as a part of the filing are only entering a best guess without the paid help of an actuary.

Once the current step is completed, please be sure to click, “Save Figures” to ensure all data is saved. Step 2 may be accessed by selecting “Step 2 >>>” at the top-left hand side of the page.

Step 2 – Health Care Insurance Plans

Step 2 – Health Care Insurance Plans

Step 2 collects insurance plan costs and enrollment for those offered to current employees and retirees. This data rolls over from what was reported the previous year. Units need to enter plan information for health plans offered. For units that indicate in Step One that it does not offer OPEB, Step 2 is optional. If the unit has plans that are only offered to active employees, those particular plans will also need to be reported.

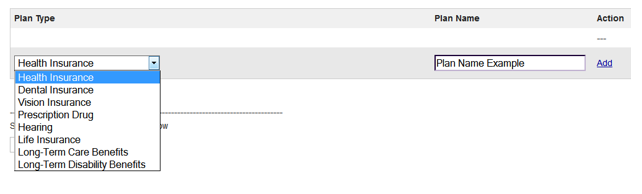

To begin, on the top of this page the user will select the appropriate plan type from the drop down menu, enter a plan name, and then click the “Add” button on the right-hand side to save the plan.

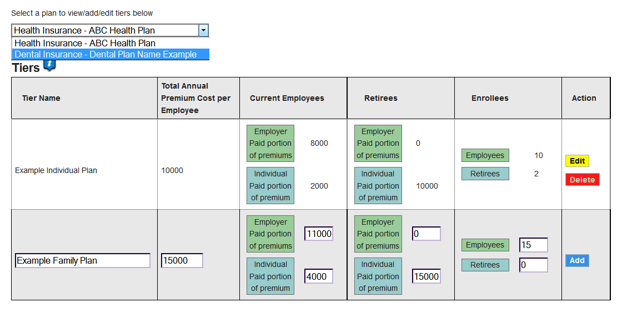

Once all applicable plans are added, the next step is to enter the cost/enrollment information for each of the plans’ tiers. After entering the annual costs and enrollment information, click the “Add” button to save the entered data. Please note that there is a drop down menu on the top left-hand side of this section that is used to navigate between each plan. At least one tier per plan must be entered.

Once all tiers, for all applicable plans, have been added, continue to the Step 3.

Step 3–Expenses

Step 3–Expenses

Step 3 summarizes the expenses incurred in the last calendar year.

The first field collects the expenditures paid directly for current retiree benefits. Examples of expenditures paid directly for current retiree benefits include payments of premiums.

The second field asks for the number of retirees currently receiving any other post-employment benefits.

The Department is also requesting an estimate of the higher premiums paid for current employees, because of the retirees in your insurance pool. If you have no current retirees purchasing health insurance, this number will be zero. For units that have not completed an actuarial valuation, please report an estimate of the higher premiums paid for current employees because of the retirees in your insurance pool.

One of the most complicated aspects of OPEB is understanding, and calculating, the subsidies provided and liability outstanding from allowing retirees to purchase health insurance on the unit’s group plan. In many cases, retirees pay the same premiums as active employees. As defined by the Government Accounting Standards Board, this can create an OPEB liability since it increases the overall risk of the plan. The true cost for retiree health coverage is usually higher than the cost for active employees. The retirees are typically older and more likely to require health care services. Therefore, this expense is a cost to the government unit, through its payment of higher premiums for current employees.

Lastly, Step 3 asks for the total OPEB expenses paid in the last year. This total represents expenses paid directly for current retirees and expenses incurred through higher premiums for current employees. This amount is typically the sum of the first and third questions in this step.

Step 4 – Liability

Step 4 – Liability

Step 4 reports factors that affect the overall OPEB liability. This step begins by collecting basic employee/retiree information followed by the last section that collects the total liability, as estimated by the unit or actuarial consultant.

In this last section of Step 4, if the unit has not completed an actuarial valuation of its OPEB liability, the Department understands that these will be estimates and the Department acknowledges that users who elect to enter these as a part of the filing are only entering a best guess without the paid help of an actuary.

The unfunded liability represents the total liability, less any assets set aside to fund future OPEB liability.

Step 5 – Assets

Step 5 – Assets

Step 5 collects information regarding the funding of retiree benefits.

The first question asks if retiree benefits are being funded with assets designated for retirees.

The next question collects the total value of assets being saved to fund future OPEB liability. If no assets are currently being saved for future OPEB liability, please enter a zero.

The last question of this report collects the total contributions during the prior year to fund future OPEB liability. If there were not any contributions in the prior year, please enter a zero.

The Sign and Submit page may be accessed by selecting “Submission >>>” at the top of the page.

Signing and Submitting the Report

Signing and Submitting the Report

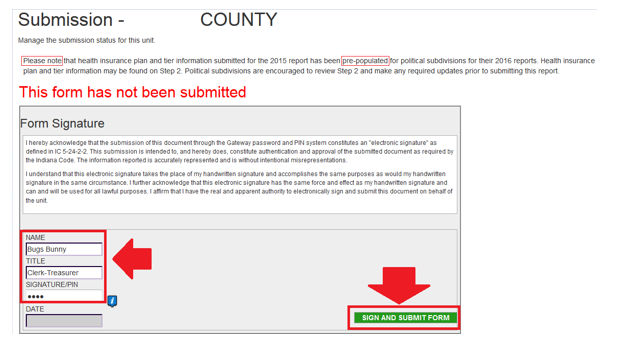

Your final step is to sign and submit this form. Please note that only users with submission rights will see the signature box.

The signature box will not appear to users with edit or read-only rights.

To sign the form, first type your name and title into the signature box. After that, you will need to enter a four-digit PIN code. This PIN code has been sent, via email, to the person with submission rights. You may contact the Department at gateway@dlgf.in.gov in the event that you have lost or not received a PIN code. Once you select “Sign and Submit Form,” today’s date will automatically populate the date field and the report will be submitted.

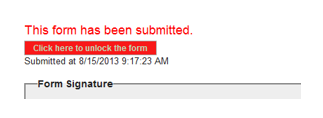

Once the form has been submitted, bold red text will state “This form has been submitted.” There will also be an unlock button that can be used to manually un-submit the form.

If you have any questions while completing this form please contact the DLGF at gateway@dlgf.in.gov or at (317) 234-4480.