Assessor Reports

Property Tax Assessment Board Of Appeals

Table of Contents

Frequently Asked Question

Frequently Asked Question

Do I access the Gateway Assessor Reports application by going to Gateway SDF? Is Gateway SDF the same as Gateway?

Assessors will access Gateway using a separate username and password than is used with GatewaySDF. Gateway’s URL is

http://Gateway.ifionline.org.

Will confidential data be submitted or accessible through this report?

The Gateway PTABOA report is a summary level report. Data on individual appeals will not be collected through the report. Furthermore, IC 6-1.1-28-12 states that confidential data should not be submitted.

Will we upload this report or manually type in the answers?

You will type in the answers.

What does “electronic submission” mean?

It means typed in and submitted via Gateway.

What is “subject year”?

We are collecting “calendar year” activity (as opposed to “assessment year” activity).

In other words, Calendar Year 2016 will be reported in the spring of 2017.

What is “some other manner” (Question 6(c))?

The Department believes that the “some other manner” option should be used relatively sparingly. Most decisions should be recorded as either in favor of the taxpayer or in favor of the assessor. In most cases, if the assessed value is reduced, the appeal would be in favor of the taxpayer. There are situations where a taxpayer appeals an assessed value and the assessed value is increased above the amount the assessor initially sets. This example would be suitable for inclusion in the “some other manner” category. Other situations may arise that warrant use of the “some other manner” option.

If the PTABOA makes a decision and it is escalated to the Indiana Board of Tax Review (IBTR), is this “resolved” (vs. open appeal)?

When the report speaks in terms of “pending” or “resolved” appeals, this contemplates appeals pending before the PTABOA or resolved by the PTABOA. An appeal may be pending before or awaiting resolution by the IBTR or Tax Court, but it is no longer pending before or awaiting resolution by the PTABOA.

Will LSA and IBTR get this report from Gateway?

The DLGF will ensure LSA and IBTR obtain a copy of the report through Gateway.

Does the DLGF collect an electronic signature on this report?

Yes. The submitter will have a four digit PIN that must be entered in order to submit the report.

What is the benefit of collecting this data? Will the data be used to insinuate poor assessor performance?

The data is valuable in assessing the efficiency of the appeals process and to identify if and where backlogs may be occurring. Legislators and taxpayers sometimes allege frustration with the length of the appeals process. This report may help identify potential improvements to the process.

What is the difference between submitter v. editor v. read-only status? Will a submitter be able to see the changes someone with edit access made before submitting?

Gateway users will have one of three access levels for the PTABOA application in Gateway. Assessors will have submission rights, which allow the user to modify all data on the report and complete the submission. Assessors may delegate editing or read-only rights to other users. Editors may update all data in the report. They cannot submit the report. Read-only users may not make any changes to report contents and may not submit the report. A submitter can review all updates made by an editor before submitting. NOTE: The Assessor is ultimately responsible for the timely submission of the report.

Does “filed with the PTABOA” mean “filed with the 133s”? Are 133s included in question 1: Notices for review?

The DLGF believes that statute requires only Form 130 appeal statistics to be documented in the report. The section of the report that captures optional information touches on property tax deductions, which would be derived from Form 133 appeals.

How do we figure out the “Total reduction in assessed valuation requested by appellants” (from optional question #1)?

Form 130 allows a taxpayer to state the assessed value they believe should be assigned to the property. The difference between the assessed values set by the assessor and the assessed values requested by the appellants would be helpful information to have. However, taxpayers do not always indicate a proposed or requested assessed value. If as a result the PTABOA believes it does not have an accurate or complete statistic on this topic, then the PTABOA can leave this question blank. Even a good-faith estimate, however, would be welcome. The PTABOA can explain the estimate in the comments section of the report.

Does this report collect data from the Form 130s and Form 133s?

The report captures information about Form 130 appeals. The “optional” responses in the report address both Form 130 and Form 133 data.

What is included in “Pending at the end of the year”?

This phrase refers to appeals that have been filed and, as of December 31 of the subject year, are awaiting either an informal meeting with the assessor or a hearing by the PTABOA.

Can you provide definitions for “In favor of” (re: Questions 6 & 7):

Statute does not define this phrase. The DLGF offers the following:

- Resolved in favor of the taxpayer: Resolved in favor of the taxpayer: If, by way of example, a taxpayer files a Form 130 appeal requesting a reduction in assessed value to $150,000 from $200,000 and the assessor or PTABOA agrees with the taxpayer and reduces the assessed value to $150,000, this would be considered a resolution in favor of the taxpayer. Furthermore, if a taxpayer requests a reduction from $200,000 but does not specify a goal assessed value, and the assessed value is reduced to $150,000, this scenario would be considered a resolution in favor of the taxpayer.

- Resolved in favor of the assessor: If, by way of example, a taxpayer files a Form 130 appeal requesting a reduction in assessed value to $150,000 from $200,000 and the assessor or PTABOA affirms the assessed value at $200,000, this would be considered a resolution in favor of the assessor. This would also include appeals that are withdrawn by the taxpayer or if the taxpayer or their representative does not show up at the PTABOA hearing and the PTABOA decides in the Assessor’s favor.

- Resolved in some other manner: If, by way of example, a taxpayer files a Form 130 appeal requesting a reduction in assessed value to $150,000 from $200,000 and the PTABOA increases the assessed value to $220,000, this could be considered a resolution in some other manner.

What do we do if taxpayers do not specify a specific assessed value they think is correct?

Please see answers to the questions above. If the assessed value is reduced, it should be recorded as a resolution in favor of the taxpayer. If the assessed value remains as originally-assessed, it should be recorded as a resolution in favor of the assessor.

Do the optional responses pertaining to deductions literally concern only deductions or do they include exemptions?

The optional responses pertain only to deductions, not exemptions.

When is the report due?

The annual report is due before April 1.

Can I amend the report after the due date?

Yes, it is permissible to amend the report after the due date; however, the report is due before April 1.

Who do I contact if I have any technical questions about the report (i.e. numbers are not saving), or need to add another staff member to edit the report?

Please contact our Gateway Support Team at Gateway@dlgf.in.gov or Billy Ottensmeyer at (317) 234-4480.

How do I get to the application screen in Gateway?

As an authorized user of the Indiana Gateway for Government Units, users will have a username and password that will allow access the program. The username is the e-mail address on file with the Department of Local Government Finance (DLGF). The DLGF will assign an initial password, which should then be changed by the owner to something unique and confidential. Users are responsible for all information entered into Gateway under the authorized user’s username and password. Users without a Gateway account may contact gateway@dlgf.in.gov to register.

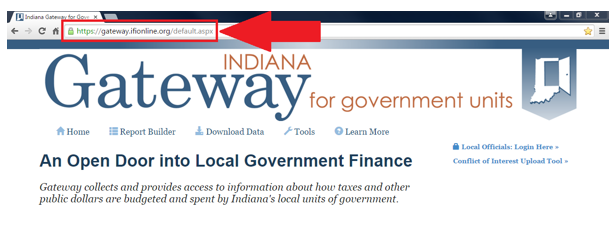

Web Address (URL):

https://gateway.ifionline.org/login.aspx

To access Gateway, open Firefox or Google Chrome and type https://gateway.ifionline.org/login.aspx into the browser, and then hit “Enter” on a standard keyboard.

Gateway works best using Firefox or Google Chrome. Internet Explorer is not a supported browser.

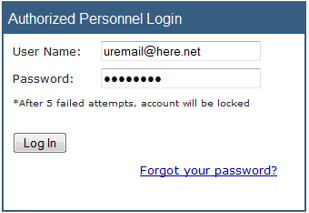

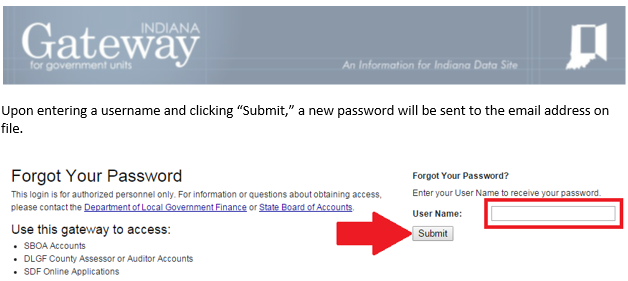

The first page users will see is the login page. Users may enter their username, which is typically the user’s email address, and account password before clicking “Log In.”

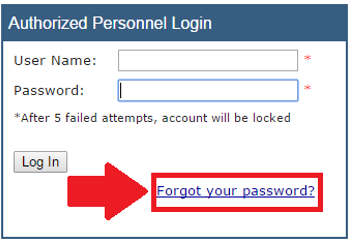

For forgotten passwords, click the “Forgot your password?” link. Users will be prompted to enter their username/email address.

Upon entering a username and clicking “Submit,” a new password will be sent to the email address on file.

Accessing the Assessor Reports application

General Information regarding Assessor Reports and its purpose.

After signing in, the user will be asked to select an application. Some of the options include the Budgets, Debt Management, and the Other Post-Employment Benefits modules. Choose the green “Assessor Reports” option in the middle column to proceed.

Each of the Gateway applications enables a local unit to submit its required forms, reports, or files to the appropriate state agency, which currently includes DLGF (Department of Local Government Finance; gateway@dlgf.in.gov), SBOA (State Board of Accounts; gateway@sboa.in.gov), IEERB (Indiana Education Employment Relations Board; gateway@ieerb.in.gov) and IGC (Indiana Gaming Commission; LDA@igc.in.gov). If questions arise about a certain agency’s form, reports, or files, please submit requests to the appropriate agency.

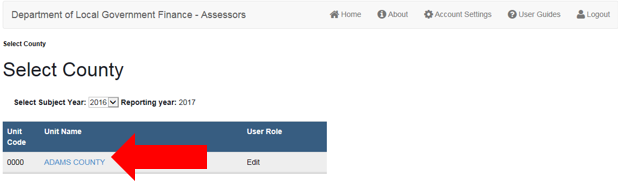

Select County from List

Once “Assessor Reports” has been selected, users may select their county from the list provided.

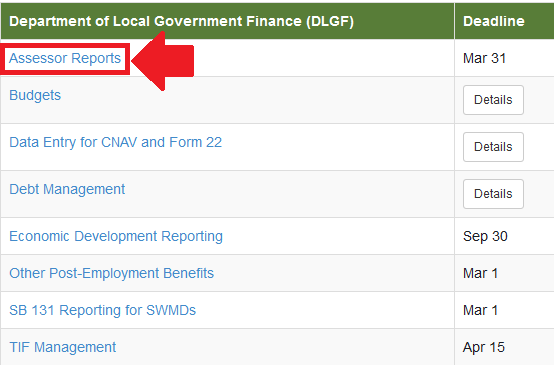

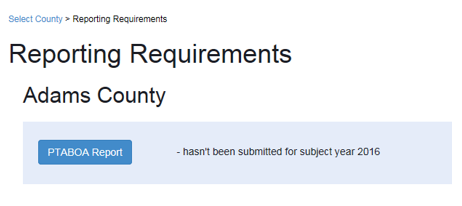

Reporting Requirements

Once the county is selected, users will be directed to a Reporting Requirements screen. At this point, users may click the blue PTABOA Report button.

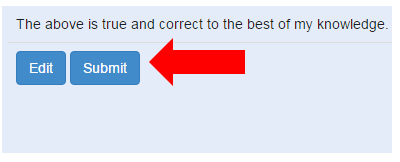

Signature of County Assessor or PTABOA Chair

Click the blue “Submit” button to get to the PTABOA Report Form Submission page.